A working hypothesis to test with a bank: When “low-risk” SMEs feel unseen, and how I plan to stress-test the claim

In an earlier post, I explored how agreement quality might be conservatively translated into financial risk without pretending we can compute it precisely (see “From Agreement Quality to Financial Risk”). This post is not a conclusion. It’s a preparatory note: a transparent snapshot of my current thinking before I speak with a bank practitioner.

This is also consistent with my CAESI approach: treat the field as a partner in inquiry, make assumptions explicit, and let practice push back before I build further. Two ideas from Leadership for Flourishing (Ritchie-Dunham et al., 2025b) help me keep the frame clean. One: organizations operate in ecosystems, and resilience often depends on the quality of relationships among customers, suppliers, partners, and institutions (Ritchie-Dunham et al., 2025a). Two: measurement is not “objective capture” but disciplined, collaborative sensemaking that makes the intangible actionable through shared intention and workable proxies (Aguilera, 2025).

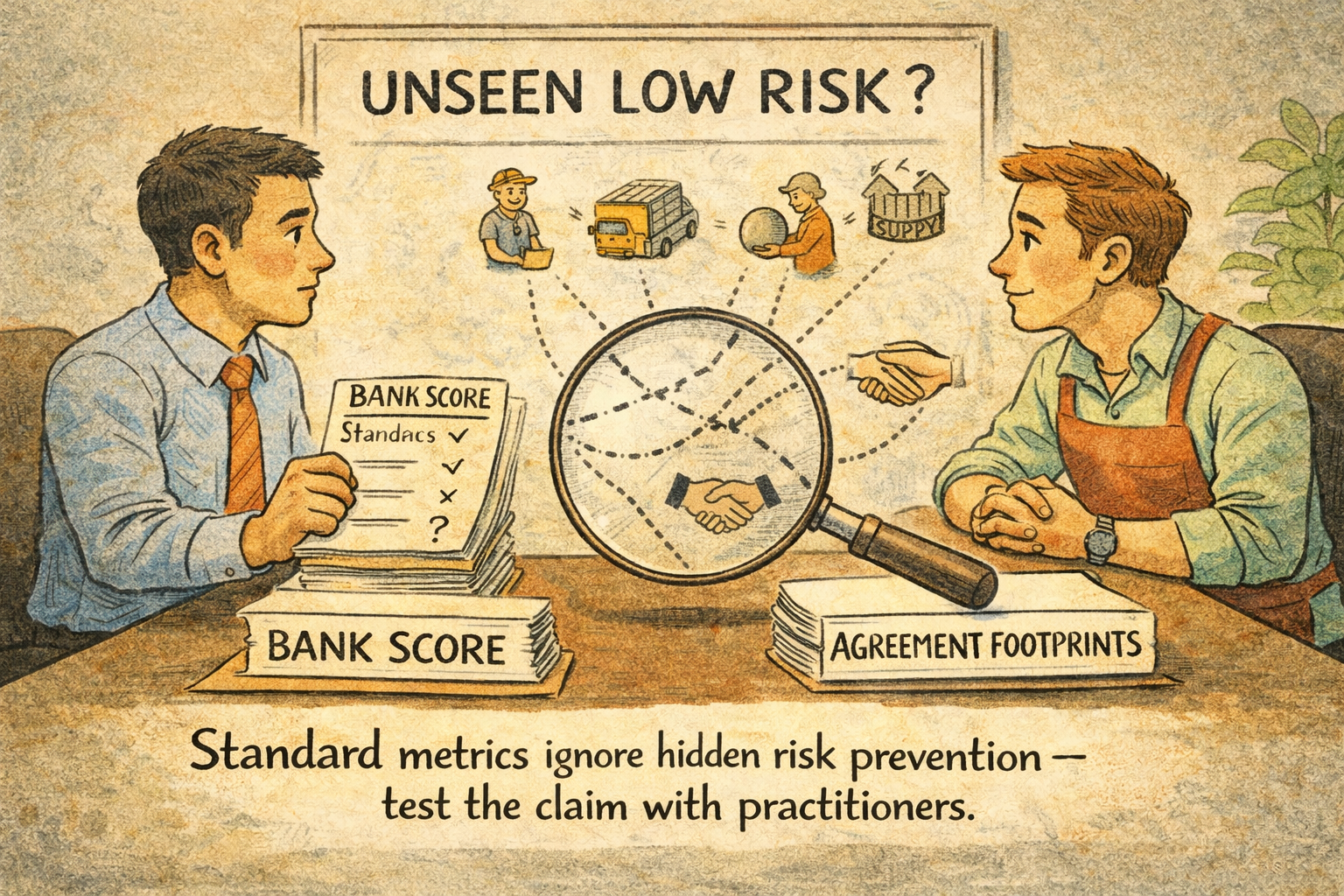

What I keep hearing (as a claim, not as truth): Across workshops, surveys, and early analysis, I keep encountering a recurring SME perception: “Banks don’t see how we prevent risk. They measure the wrong things. They don’t understand us.” I’m deliberately not treating this as evidence. It’s a claim from one side of the relationship. It may be accurate, partly accurate, or strategically biased. My job is to test it.

The twist I want to test (not yet a conclusion)

The firms raising this claim are often not the ones that are obviously reactive. It is frequently firms that describe themselves as intentionally building strong agreement systems: clear handovers, early problem surfacing, disciplined coordination with suppliers and customers, and compounding learning routines. In other words, firms that appear closer to the “more anticipatory” minority in many SME ecosystems. Their claim is not: “We are failing.” Their claim is: “We are stable because of how we coordinate, and that stability is hard to communicate in a way that counts.”

This sets up a working hypothesis: H1 (legibility hypothesis): Some SMEs with strong risk-prevention capability feel “unseen” because their capability resides in ecosystem coordination and agreement health, real but not always easy to evidence in standardized credit workflows. There is also a second hypothesis embedded in their story that I do not assume to be true. Still, I want to test whether practitioners recognize the possibility: H2 (incentive tension hypothesis): Under certain conditions, requests for short-term performance improvement could unintentionally compete with the routines and agreements that make an SME resilient in the first place. I’m not attributing this to “banks.” It’s a general systems possibility: when evidence channels reward specific signals, actors adapt.

What does “risk prevention capability” mean in plain operational terms

When SMEs talk about preventing risk through their way of working, they often point to observable patterns at ecosystem interfaces:

Interfaces don’t leak: customer requirements, supplier specs, handovers, and responsibilities are clear enough to avoid rework.

Agreements stay negotiable: issues surface early because assumptions can be renegotiated before damage accumulates.

Learning compounds: insights become shared routines across teams and key partners, not isolated “lessons learned.”

Coordination is visible: decisions, exceptions, and accountability are handled in ways that reduce surprises.

This is operational. It’s just not always “paper-evidence shaped.”

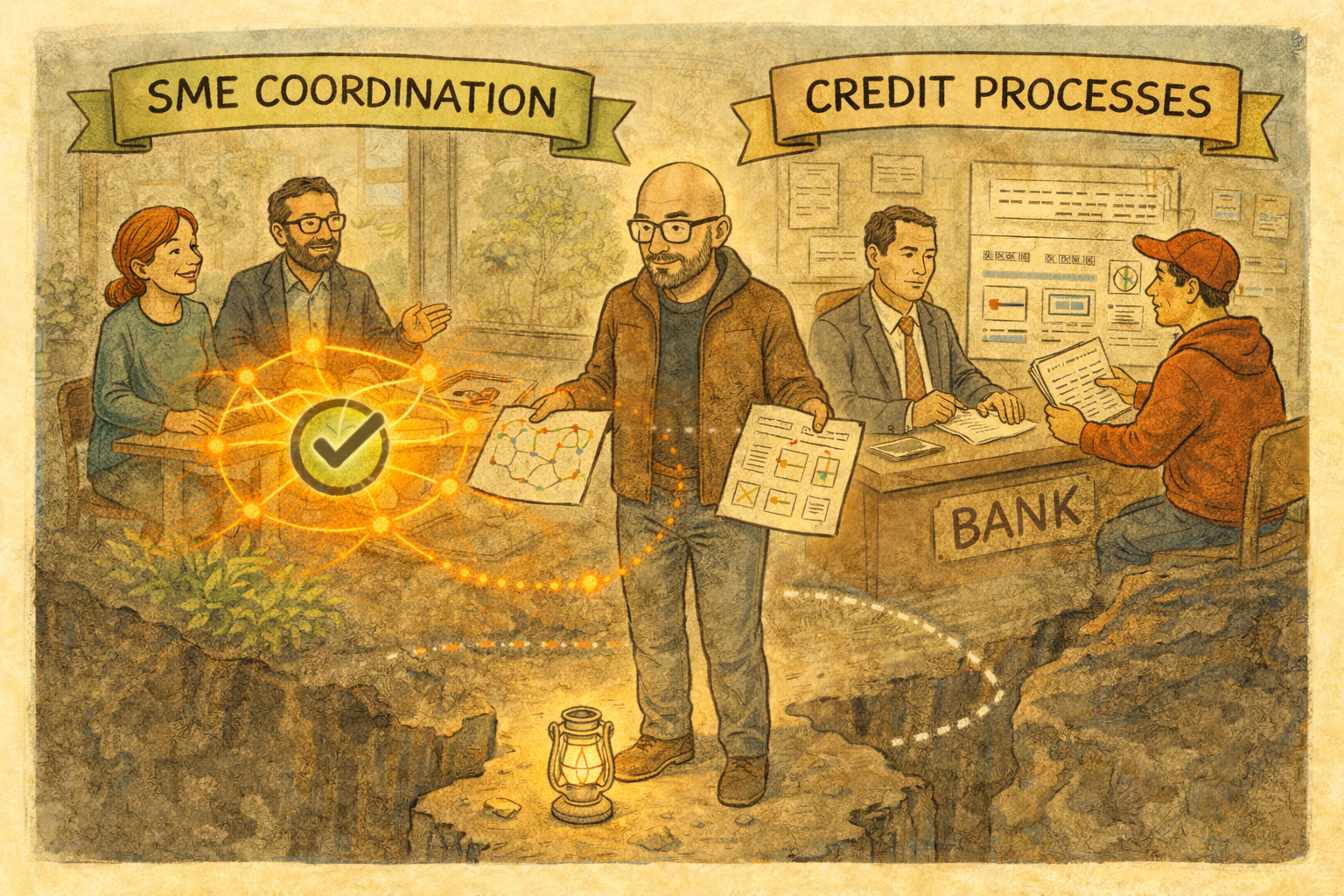

If H1 is even partly true, the real issue is not “bank ignorance” or “SME complaining.” It’s measurement and legibility. Aguilera’s point helps here: measurement begins with shared intention and then builds proxies that are “good enough” for decision-making (Aguilera, 2025). My intention in the upcoming conversation is modest: Can I learn how practitioners currently make non-financial risk-prevention signals legible, without creating theater or pretending to be precise? I’m not proposing a solution yet. I’m trying to understand reality.

What I will do (first step: a short, bounded practitioner check-in)

I’m starting with a short check-in with a bank.

no client files

no confidential data exchange

no recordings

no identifiable reporting

The purpose is to test recognizability and learn current practice, not to “validate” my research.

The questions I’ll bring (to test H1 and H2 without bias)

I’m bringing two types of questions: recognition and practice.

Recognition

Do you recognize the pattern that some SMEs feel “unseen” in how they prevent risk?

If yes, what typically drives that perception?

Practice

In your daily work, what do you already look for beyond financials to gauge a company's risk-prevention capabilities?

Which non-financial signals are credible enough to trigger a deeper conversation, without being fooled by a good story?

Are there situations where well-meaning performance requests could conflict with resilience routines, and if so, how do you notice and handle that?

I’m especially interested in the “how do you avoid being seduced by narrative?” question because it’s the honest counterweight to the SME claim.

What success looks like (at this stage)

Success is not “being right.” It’s improving the quality of my next step:

If practitioners say, “We don’t recognize this at all,” I revise the hypothesis.

If they say: “We recognize it, but it’s hard to evidence,” I focus on legibility mechanisms.

If they say, “We recognize incentive tensions,” I can explore that carefully later, without blaming anyone.

If the meeting never happens, despite positive initial reactions, I know I have to work on my science communication skills.

This is preparation. The actual learning happens in the conversation.

References

Aguilera, H. (2025). Collaborative measurement of flourishing. In J. L. Ritchie-Dunham, K. E. Granville-Chapman, & M. T. Lee (Eds.), Leadership for flourishing. Oxford University Press. https://doi.org/10.1093/9780197766101.003.0014

Ritchie-Dunham, J. L., Dinwoodie, D., & Maczko, K. (2025a). Organizational ecosystems of flourishing. In J. L. Ritchie-Dunham, K. E. Granville-Chapman, & M. T. Lee (Eds.), Leadership for flourishing. Oxford University Press. https://doi.org/10.1093/9780197766101.003.0009

Ritchie-Dunham, J. L., Granville-Chapman, K. E., & Lee, M. T. (Eds.). (2025b). Leadership for flourishing. Oxford University Press. https://doi.org/10.1093/9780197766101.001.0001